Long Centene Corporation ($CNC)

The Bullish Case for ($CNC)

The healthcare sector has been a battleground of regulatory shifts, cost pressures, and evolving consumer demands since Trump’s inauguration. Yet, within this landscape, Centene Corporation ($CNC) stands out as a compelling re-valuation opportunity.

Here’s why I believe $CNC presents a strong bullish case:

1. A Dominant Player in Government Healthcare

Centene operates as a leading managed care company with a dominant presence in Medicaid, Medicare, and Affordable Care Act (ACA) exchanges. With over 28 million members, it is one of the largest Medicaid providers in the U.S., benefiting from federal and state funding. As Medicaid expansion continues and government reliance on private insurers grows, Centene is poised to capture more market share.

2. Medicaid Redetermination Risks Overblown

One of the biggest concerns surrounding Centene has been the Medicaid redetermination process, where states reassess Medicaid eligibility following the expiration of pandemic-era enrollment protections. This has led to some member attrition, but the impact appears to be less severe than initially feared.

Additionally, many of the members losing Medicaid coverage are transitioning to ACA exchange plans, where Centene remains a leading provider. This partially offsets the enrollment losses, reinforcing the stickiness of its customer base.

3. Trump's Risk with Direct Order Government Entities (DOGE) for CNC

One of the key risks for Centene is the Trump administration is the prospect of Direct Order Government Entities (DOGE) being expanded to increase price competition in government healthcare programs. Trump has historically been vocal about reducing costs in government healthcare, favouring policies that could drive pricing pressures on managed care providers like Centene.

If Trump pursues Medicare Advantage reforms or expands direct government healthcare contracting, this could put downward pressure on CNC's margins. However, Centene’s extensive Medicaid and ACA footprint, which are politically more difficult to overhaul, provides some insulation. Additionally, Centene’s cost-control initiatives and scale advantages should help mitigate potential pricing headwinds from increased government competition.

While Trump's policies pose a headline risk, the structural demand for managed care solutions remains robust, particularly as state-level decisions play a more dominant role in Medicaid expansion and ACA administration. Thus, while the risk is real, Centene's diversified positioning should help absorb any potential policy shifts.

4. Margin Expansion & Cost Control Initiatives

Over the past few years, Centene has embarked on an ambitious margin improvement program, focusing on reducing administrative expenses, optimizing claims management, and divesting non-core assets. The company is targeting a 15% adjusted operating margin by 2025, a significant improvement from its current levels.

Key drivers of this margin expansion include:

Operational efficiencies: Streamlining costs and eliminating redundancies in acquired businesses.

Medical Cost Management: Leveraging data analytics to control costs and enhance underwriting discipline.

Divestitures: Shedding non-core assets to focus on its most profitable segments, such as the recent sale of its international business.

5. Strong Cash Flow & Shareholder Returns

Centene’s business model generates robust cash flows, which are being strategically deployed to enhance shareholder value. The company has consistently used excess capital for:

Debt reduction, improving financial flexibility.

Stock buybacks, returning capital to shareholders while maintaining a disciplined balance sheet.

Strategic acquisitions, reinforcing its presence in key markets.

With a projected $5 billion in operating cash flow in the coming years, Centene is well-positioned to fund both growth and shareholder-friendly initiatives.

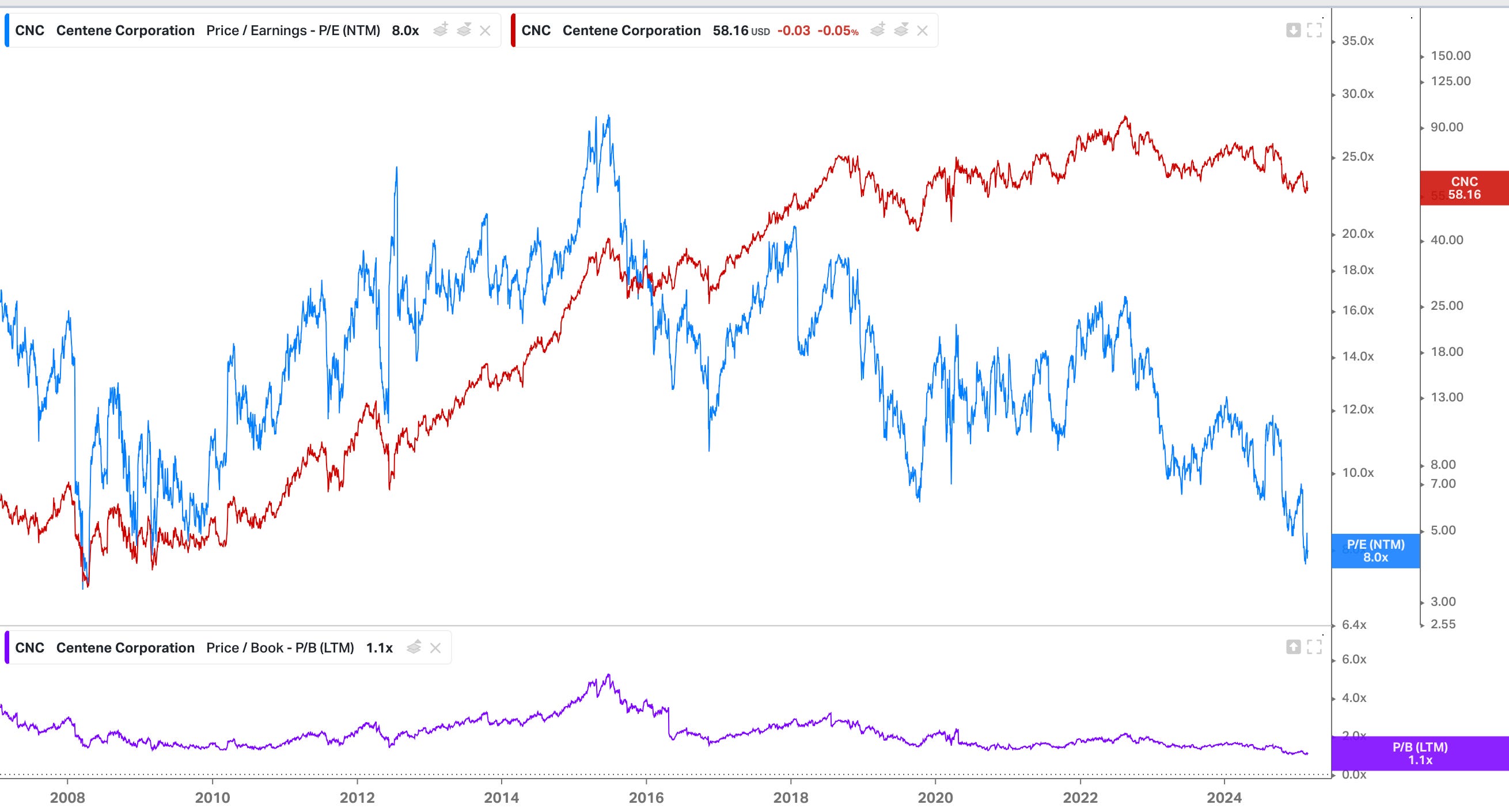

6. Valuation Upside & Underrated Growth

Centene is trading at one of the lowest earnings ratios in its history which signals that investors are very pessimistic. Despite its strong fundamentals, Centene trades at a discount to its peers in the managed care space. At ~8x forward earnings, it offers an attractive entry point compared to larger competitors like UnitedHealth Group ($UNH) and Elevance Health ($ELV), which trade at higher multiples.

Key valuation arguments:

Earnings Growth: EPS is expected to grow double digits over the next few years.

Stable Revenue Base: With Medicaid and ACA membership driving recurring revenues, Centene’s financials remain relatively insulated from economic cycles.

Multiple Expansion Potential: As execution on margin improvements progresses, there’s room for valuation re-rating closer to peers.

Share Repurchase Program: They have repurchased over $2B in 2024 and expected to repurchase $3B or 10% of the market cap in 2025.

Centene at these prices could very well deliver some great returns in the following years but investors need to remain patient and manage the increase in volatility.

Disclosure: I am long Centene at 56.7.